Vladimir Putin went to war with an economy that could not sustain the conflict. Everyone knew this. The intelligence agencies knew it. The Russian finance ministry knew it. Western analysts certainly knew it.

What nobody fully expected was how quickly the structural damage would become irreversible. Three years into the Ukraine invasion, russia war economic impact has moved beyond recession. It has entered territory that looks more like systemic breakdown.

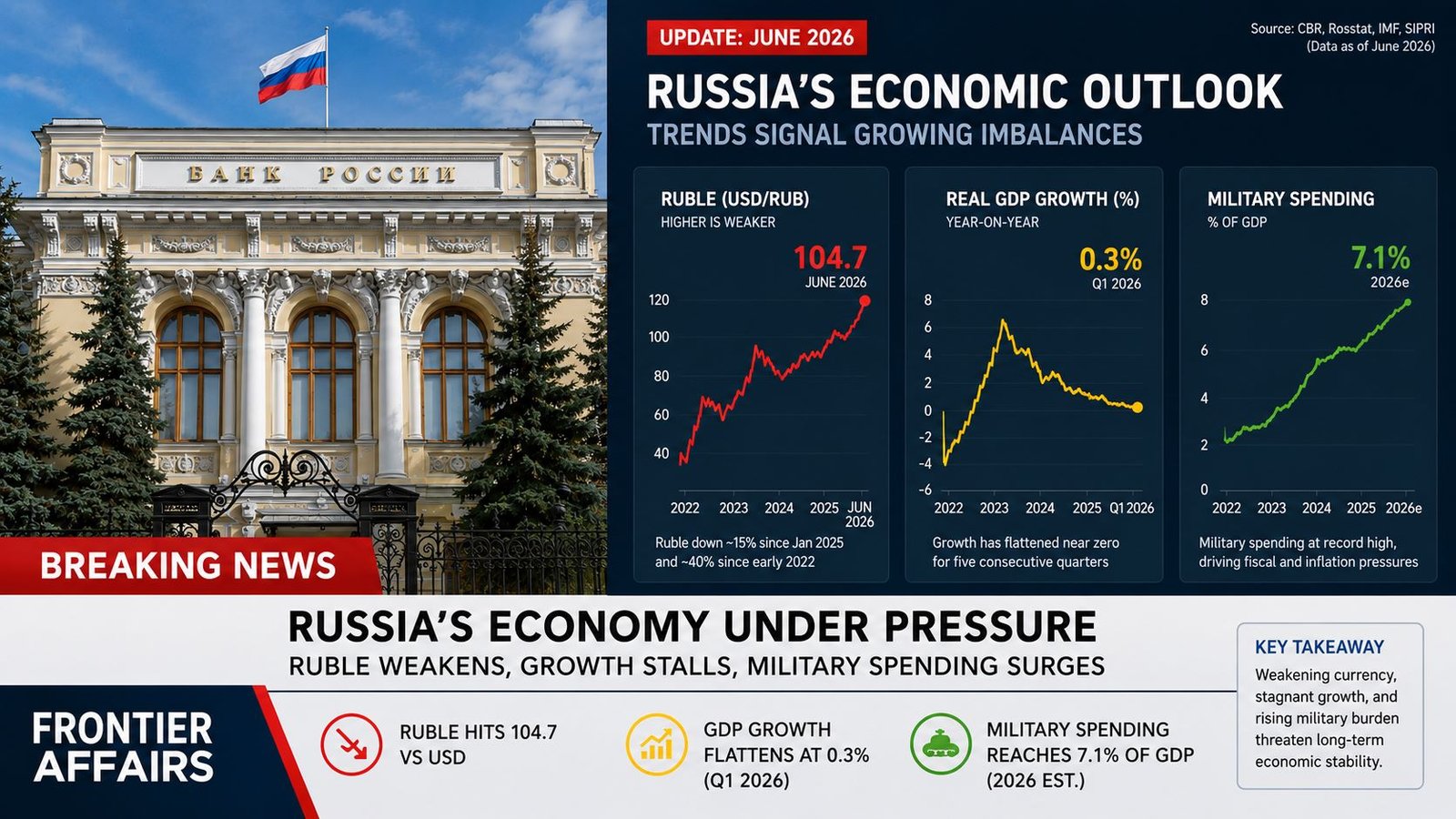

The ruble has collapsed in real terms. Military spending has consumed the state budget. Oil revenues have evaporated. The productive capacity of the economy is shrinking. Capital flight continues despite controls. The next five years will determine whether Russia rebuilds or simply manages decline.

This is not speculation. The numbers are documented. The trajectory is clear.

What is less clear is whether Putin understands the scale of the damage his own decisions have created.

The Military Spending Trap

Here is where the story begins. A simple accounting problem.

Russia’s military budget in 2023 was roughly 86 billion dollars. By 2026, estimates place it at 120-140 billion dollars annually. That is 30-40 percent of total federal spending on military operations and equipment.

For context: the United States military budget is about 800 billion dollars annually. The U.S. economy is roughly 15 times larger than Russia’s. The American military spending to GDP ratio is around 3 percent.

Russia’s ratio has reached 6-7 percent of GDP. Some estimates place it higher.

The Budget Mathematics

This creates a mathematical problem with no clean solution. Russia’s total federal budget is roughly 280 billion dollars.

One-third of that goes to military spending. Another third goes to social spending pensions, healthcare, education. Another third goes to bureaucracy and debt servicing.

That leaves almost nothing for infrastructure. Almost nothing for investment in civilian industry. Almost nothing for economic modernization.

The Weapon of Last Resort

When a government cannot balance its budget, it prints money. Russia did exactly this.

The Central Bank expanded the monetary base dramatically. This created inflation. The Central Bank then raised interest rates to combat inflation. High interest rates crushed investment and consumer spending.

This is the trap. Military spending forced monetary expansion. Monetary expansion destroyed purchasing power. Economic destruction meant less tax revenue. Less tax revenue meant more spending pressure on the budget.

Russia entered a cycle it cannot escape.

Oil Revenue Collapse: The Energy Shock

Russia’s economy was never primarily about diversified industry. It was always primarily about energy export.

In the decade before the Ukraine invasion, energy exports represented roughly 40 percent of federal government revenue. More than half of Russia’s export earnings came from oil and natural gas.

Then came Western sanctions targeting russian oil revenue directly.

The Shadow Fleet Strategy

The EU implemented a price cap on Russian oil at 60 dollars per barrel. Simultaneously, it banned direct purchases of Russian crude. This should have devastated Russian energy sales.

Instead, Russia developed a workaround: the shadow fleet.

Russian energy companies purchased old tanker ships many purchased from scrapyards or from Cyprus, Malta, and other neutral shipping registries. These ships, renamed and flagged under obscure jurisdictions, transport Russian oil to China, India, and other non-sanctioning nations.

Shadow fleet sanctions have become increasingly aggressive. Western nations have targeted insurance, maritime brokers, and port access. But the workaround persists.

Russia’s oil still flows. The price remains depressed. The revenue remains insufficient.

The BRICS Alternative That Isn't

Putin has pivoted toward BRICS particularly China and India. Both countries will purchase Russian oil. Both are willing to work around sanctions constraints.

But here is the catch: neither country is willing to pay premium prices. India negotiates discounts of 20-30 percent below global prices. China does the same.

Russia’s energy revenue is therefore simultaneously flowing and collapsing. The volumes are there. The price is not.

This cannot sustain the military budget.

The Ruble Collapse: Currency as Economic Signal

The ruble tells the real story of russia war economic impact more honestly than any other metric.

In early 2022, before the invasion, one dollar cost roughly 75 rubles. By mid-2024, it cost 110 rubles. In 2026, the official exchange rate hovers around 100-105 rubles per dollar. But the black market rate is considerably worse closer to 130-150 rubles per dollar depending on location and liquidity.

That is not a technical adjustment. That is a currency in structural decline.

Why the Ruble Collapsed

The collapse has multiple drivers. Capital controls prevent Russians from moving money out of the country legally. So they move it illegally through cryptocurrency, through intermediaries, through informal networks.

Capital outflows reduce ruble demand. Reduced demand means depreciation.

Simultaneously, Russia’s imports have become more expensive. Russian businesses need foreign currency to buy components from countries that will still trade with them. That demand for foreign currency also depresses the ruble.

The Central Bank tried to support the currency by raising interest rates. High rates made borrowing expensive. Expensive borrowing contracted the economy further.

Why the Ruble Collapsed

When a currency collapses, inflation follows. Inflation erodes purchasing power. Eroded purchasing power means reduced real wages.

The average Russian’s purchasing power in 2026 is substantially lower than in 2021 despite nominal wage increases. This matters politically. It matters socially.

Russians who were middle class in 2021 are struggling in 2026. The elderly on fixed pensions have been devastated. Consumer spending has contracted. Consumer spending contraction means less demand for goods and services. Less demand means business failures and layoffs.

Sanctions Effectiveness: The Structural Squeeze

Western sanctions against Russia were never designed to end the war overnight. They were designed to create structural economic pressure that would, over time, become unsustainable.

This strategy is working. Not quickly. But it is working.

The Technology Squeeze

Russia has been cut off from advanced semiconductor technology. It has been cut off from precision manufacturing equipment. It has been cut off from aerospace components and advanced materials.

Russia has workarounds. But workarounds are inferior to direct access.

Russian businesses must now source technology through Iran, through China, through Central Asian intermediaries. Each layer of intermediary adds cost and delay. Quality suffers. Price increases.

This affects military production. It affects civilian industry. It affects infrastructure maintenance.

The Trade Diversion

Russia has reoriented its trade toward non-sanctioning nations. But the scale of trade available in these alternative markets is smaller than what Russia lost.

The European Union was Russia’s largest trading partner before sanctions. The EU market is closed now. Russia can export to China, India, Iran, Turkey. These markets combined are significantly smaller than the EU market was.

Supply and demand tells the rest. Fewer customers means lower prices. Lower prices means lower revenue.

Russia Iran Trade as Desperation Signal

The deepening of russia iran trade in 2024-2026 is particularly instructive. Russia and Iran have formed what amounts to an alternative economic bloc. Each is sanctioned by the West. Each needs access to markets and technologies the other can theoretically provide.

In practice, what this means is that Russia is trading oil for Iranian drones. Russia is providing technology assistance to Iranian nuclear programs in exchange for rare earths and petrochemicals.

This is not strategic partnership. This is mutual desperation.

The GDP Question: How Bad Is It Really?

Russia’s official GDP figures should be taken with extreme skepticism. The Russian government has every incentive to misrepresent economic performance.

Western estimates place russian gdp 2026 at roughly 1.8-1.9 trillion dollars down from roughly 1.9-2.0 trillion in 2021. That is stagnation at best, contraction at worst.

But those are nominal figures. Adjusted for inflation and currency depreciation, real GDP has likely contracted 10-15 percent since 2021.

The Investment Collapse

Russia's domestic investment has collapsed. Businesses are not building new factories. They are not upgrading equipment. They are not investing in technology.

Why? Because nobody knows what the economic environment will look like in 2-3 years.

Capital makes long-term investments when the future looks stable. Russia's future looks uncertain. Capital therefore sits idle or flees.

This self-reinforces economic decline. Less investment means lower productivity growth. Lower productivity growth means lower wages. Lower wages mean less consumption. Less consumption means less business investment.

Putin's Strategic Miscalculation

Here is the uncomfortable reality: Putin appears to have believed that Western sanctions would be temporary.

The assumption seems to have been that Western unity would fracture. That economic pressure on Europe would force the EU to lift sanctions. That time was on Russia’s side.

Three years later, Western unity has held. Sanctions have expanded rather than contracted. Russia’s economy has deteriorated rather than stabilized.

The Sunk Cost Trap

Russia is now trapped in what economists call a sunk cost dynamic. The government has already committed enormous resources to the war. The infrastructure has been destroyed. The military has suffered massive casualties.

Withdrawing would mean admitting that all of this was for nothing. Politically, Putin cannot do this. Economically, Russia cannot continue indefinitely.

This creates a trapped equilibrium. Russia cannot win. Russia cannot withdraw. Russia is therefore committed to a slow grinding attrition that will continue to hollow out the economy.

The Long-Term Damage

Some of this damage is reversible. Some is not.

Equipment can be rebuilt. Factories can be retooled. Capital can return if investment conditions improve.

But human capital flight may not be reversible. The educated, the young, the ambitious have left Russia in significant numbers since 2022. They are working in Europe, in the Middle East, in Central Asia. They are building careers outside Russia.

When Russia eventually seeks to rebuild its economy, a generation of talent will be permanently lost.

The Road Ahead: No Good Outcomes

Russia faces a structural economic problem with no painless solution.

If Russia ends the war and accepts territorial losses, Putin’s political legitimacy faces an immediate challenge. Continuing the war sustains the military-political coalition but accelerates economic decline.

If Russia attempts to negotiate a settlement that preserves territorial gains, it will face Western demands for reparations and sanctions relief only under strict conditions. This may be politically acceptable to Putin but economically insufficient for Russia’s needs.

If Russia continues the current trajectory military spending at 6-7 percent of GDP, sanctions in place, capital flight continuing the economy will continue to decline. By 2030, Russia’s purchasing power may have contracted 25-30 percent from 2021 levels.

That creates internal political pressure. Economic decline eventually creates political instability. Military payrolls become harder to meet. Social spending becomes harder to maintain. Resentment accumulates.

None of these paths lead to the outcome Putin wanted.

Do you think Russia’s economy can sustain its current military spending trajectory, or is economic collapse inevitable within 5 years?

Related News

SAVE America Act 2026: Four Republicans Block Trump’s Voter ID Bill in Senate

Russia War Economic Impact: How Putin Broke His Own Economy

Starmer Mandelson Epstein: What the New Files Really Reveal